From a very early age he developed the

extraordinary ability to solve complex mathematical problems by using geometrical

visualisation. This all happened during turbulent times: Mandelbrot and his

Jewish-Lithuanian family emigrated to Paris in 1936 before the outbreak of the

Second World War. These experiences helped to shape his mathematical talent, which

“I developed by observing plants and trees while we were fleeing.” In 1944 he passed

the entrance exam for the École Polytechnique in Paris with flying colours. “The

problem that we were set was easy to solve if you used spherical coordinates instead

of Cartesian ones. But I was the only candidate in the whole of France who was able

to see that at the time.”

Mandelbrot began his career in the United States in the late 1950s, working in

the research department of the Thomas J. Watson Research Center at IBM. Looking

back on a career spanning a total of 35 years at the computer giant, Mandelbrot

– who eventually became a professor of mathematics – described this period as a

‘golden age’: “I found fulfilment in seemingly unrelated areas that did not

follow any usual pattern and were therefore widely regarded as bizarre.”

He was not universally understood. Throughout his life, Benoît Mandelbrot was

seen as something of a maverick in the world of mathematics. He remained an

unorthodox lone voice, a contrarian and a non-conformist, attaching little

importance to formal theorems and proof.

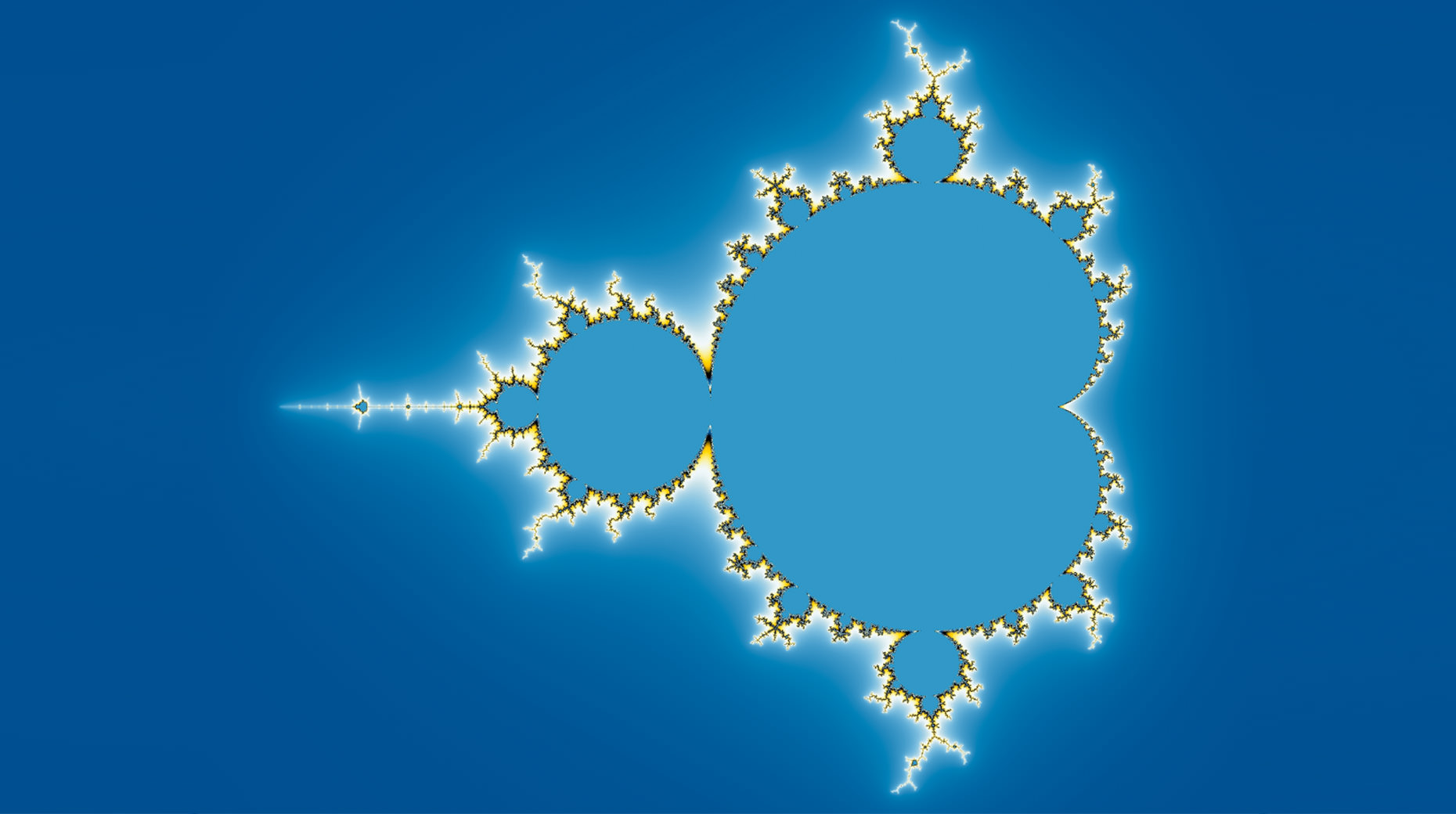

The Mandelbrot set

Even when he was growing up, Mandelbrot had admired Johannes Kepler, the German

natural philosopher, mathematician, astronomer and astrologist. Kepler had used

his interdisciplinary knowledge to devise three laws of planetary motion. As a

young person, Benoît B. Mandelbrot dreamed of discovering something of similarly

far-reaching importance. And he succeeded in doing just that when he developed

the Mandelbrot set that is named after him. This set represents a pattern that

can be used to calculate and visualise the roughness repeatedly occurring in

nature as fractals. This happened in 1978 with the computer animation that

became known as fractals, and these most intricate of geometric shapes described

by the Mandelbrot set show that fractals and roughness – despite their many

differences – reveal a few common characteristics.

If you zoom in and look more closely, you can see how the same smaller and

smaller intricate shapes and patterns are successively nested inside each other

and repeat infinitely. The contour of a section of a fractal – no matter how

small – will always look like a coastline. The fractal dimension is a ratio

introduced by Mandelbrot which, for the first time, enabled the roughness and

complexity of shapes – and even of non-linear events – to be described in

quantitative terms. The peculiar thing about the intricate and complex shapes

and patterns of fractals is that the underlying equation is anything but

complicated for mathematicians: f(z) = zn² + c. The Mandelbrot set

‘M’ is the set of all complex numbers ‘c’ for which the recursively defined

sequence of complex numbers z0, z1, z2,... with

the formation law zn+1 := zn² + c and the initial

condition z0 := 0 remains bounded, i.e. the amount of the sequence

members does not grow beyond all limits.

Markets between risk, reward and ruin

Nowadays these findings are used in areas such as medicine, geosciences,

seismology, image processing and special effects in cinematography. But the

financial services industry has also been able to learn lessons from these

findings: if market participants had listened to Benoît B. Mandelbrot more often

in recent decades, they probably would not have been so frequently caught

off-guard by turbulent events. The inventor of fractal geometry compared the

actors in financial markets with sailors. If these seafarers build a ship, they

are not thinking about when exactly the next storm will be coming. They build

their ship in such a way that it is sufficiently robust to withstand any

conceivable storm. Financial market players, on the other hand – according to

Mandelbrot – behave as if it were sunny every day. They calculate their ability

to sustain risk based on a confidence level of 99 per cent or even 99.5 per

cent, thereby ignoring the extreme events (‘fat tails’) that will sink the ship

during a storm. Mandelbrot never tired of repeatedly pointing out that the

models used in practice systematically underestimate the true risks. He

considered financial market theory to be a ‘phoney science’, believing that

market gains and losses were determined by extreme events rather than by

‘normal’ price fluctuations. He proved that financial market price volatility

could be described not by normal distribution but by Lévy distribution, which in

theory – like the Mandelbrot set – exhibits infinite variance.

On the other hand, Gaussian distribution – the probability function widely

established up to that point – regularly caused statisticians, climate

scientists and capital market participants to fall into the same trap: they

assumed that probabilities exhibit a bell-curve distribution and that the larger

the deviations from a norm are, the less frequently they occur. And this was

where they often went wrong, as Benoît B. Mandelbrot explained more than two

years before the great financial crisis – at the first risk management

conference held by Union Investment in 2006. “The stock market crash of 19

October 1987 should never have happened,” was Mandelbrot’s view. According to

calculations based on normal distribution, the probability of a one-day loss of

almost 30 per cent on the Dow Jones was 1 to1050 – a one followed by

50 zeros.

As far as the normal-distribution assumption was concerned, Mandelbrot was also

critical of the widely used risk metric ‘Value at Risk’. “Don’t make me laugh.

You believe that Value at Risk can quantify the potential risk? ... If you look

at how the risk of various financial products is measured, you will find that

virtually all evaluations are based on the assumption of normal distribution.

That is why risk is systematically underestimated. I hope that my theory of

fractals will one day be as easy to use as normal distribution. Then you will

see that the risk is actually much greater.” Mandelbrot was convinced that most

risk theoreticians had been heading down the wrong path. “My entire life has

been spent studying risk,” was his assessment. Benoît B. Mandelbrot gave his

final lecture in the spring of 2010, concluding with the words: “Bottomless

wonders spring from simple rules, which are repeated without end – again and

again.” The father of the Mandelbrot set and fractal theory died in Cambridge,

Massachusetts, in the United States on 14 October 2010. He opened our eyes to

the fact that fractals form the core of life and that, behind the apparent chaos

of roughness, an impressive order exists. Thanks to his fractal geometry we can

now understand the Book of Nature a little better.